SHARE THIS PAGE

Register 2 months in advance and save $500.

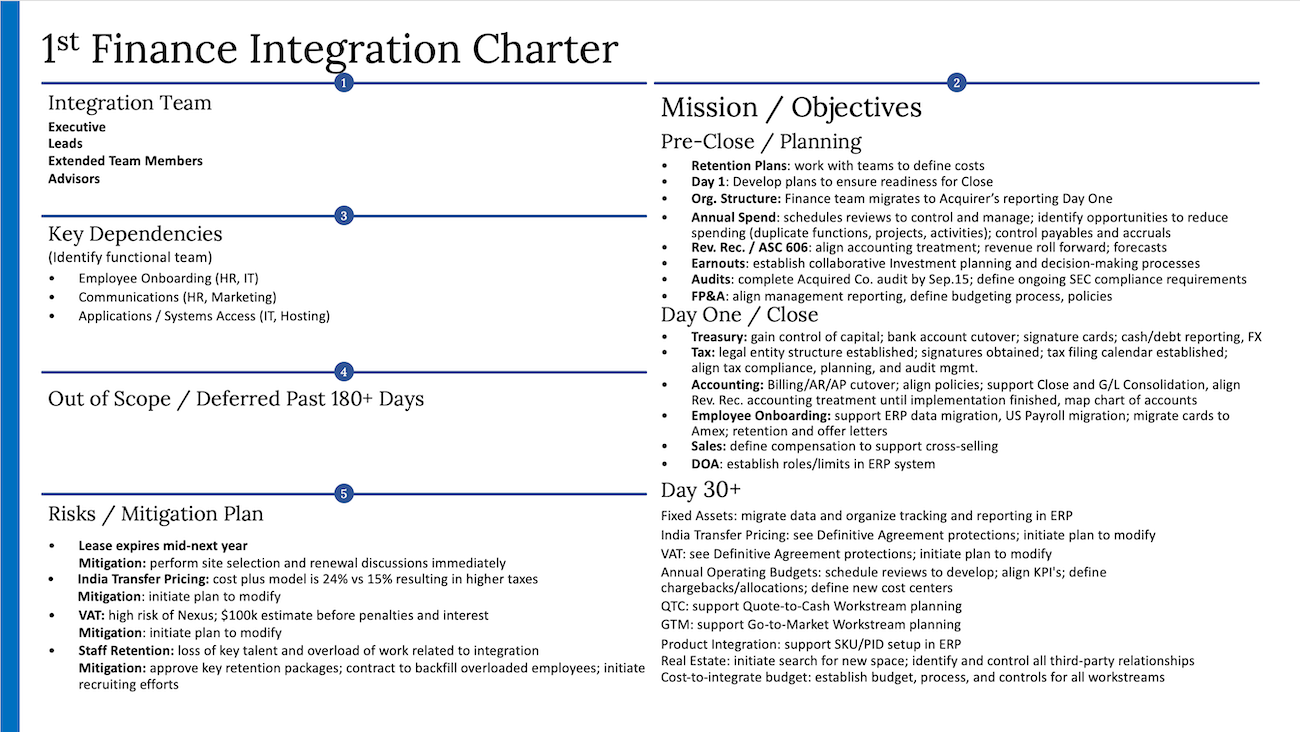

1st Finance Integration Charter

Mission / Objectives

Pre-Close / Planning

- Retention Plans: work with teams to define costs

- Day 1: Develop plans to ensure readiness for Close

- Org. Structure: Finance team migrates to Acquirer's reporting Day One

- Annual Spend: schedules reviews to control and manage; identify opportunities to reduce spending (duplicate functions, projects, activities); control payables and accurals

- Rev. Rec. / ASC 606: align accounting treatment; revenue roll forward; forecasts

- Earnouts: establish collaborative Investment planning and decision-making processes

- Audits: complete Acquired Co. audit by Sep. 15; define ongoing SEC compliance requirements

- FP&A: align management reporting, define budgeting process, policies

Day One / Close

- Treasury: gain control of capital; bank account cutover; signature cards; cash/debt reporting, FX

- Tax: legal entity structure established; signatures obtained; tax filing calendar established; align tax compliance, planning and audit mgmt.

- Accounting: Billing/AR/AP cutover; align policies; support Close and G/L Consolidation, align Rev. Rec. accounting treatment until implementation finished, map chart of accounts

- Employee Onboarding: support ERP data migration, US Payroll migration; migrate cards to Amex; retention and offer letters

- Sales: define compensation to support cross-selling

- DOA: establish roles/limits in ERP system

Day 30+

- Fixed Assets: migrate data and organize tracking and reporting in ERP

- India Transfer Pricing: see Definitive Agreement protections; initiate plan to modify

- VAT: see Definitive Agreement protections; initiate plan to modify

- Annual Operating Budgets: schedule reviews to develop; align KPI's; define chargebacks/allocations; define new cost centers

- QTC: support Quote-to-Cash Workstream planning

- GTM: support Go-to-Market Workstream planning

- Product Integration: support SKU/PID setup in ERP

- Real Estate: initiate search for new space; identify and control all third-party relationships

- Cost-to-integrate budget: establish budget, process, and controls for all workstreams

Integration Team

- Executive

- Leads

- Extended Team Members

- Advisors

Key Dependencies (identify functional team)

- Employee Onboarding (HR, IT)

- Communications (HR, Marketing)

- Applications / Systems Access (IT, Hosting)

Out of Scope / Deferred Past 180+ Days

No items currently listed.

Risks / Mitigation Plan

- Lease expires mid-next year

Mitigation: perform site selection and renewal discussions immediately - India Transfer Pricing: cost plus model is 24% vs 15% resulting in higher taxes

Mitigation: initiate plan to modify - VAT: high risk of Nexus; $100k estimate before penalties and interest

Mitigation: initiate plan to modify - Staff Retention: loss of key talent and overload of work related to integration

Mitigation: approve key retention packages; contract to backfill overloaded employees; initiate recruiting efforts

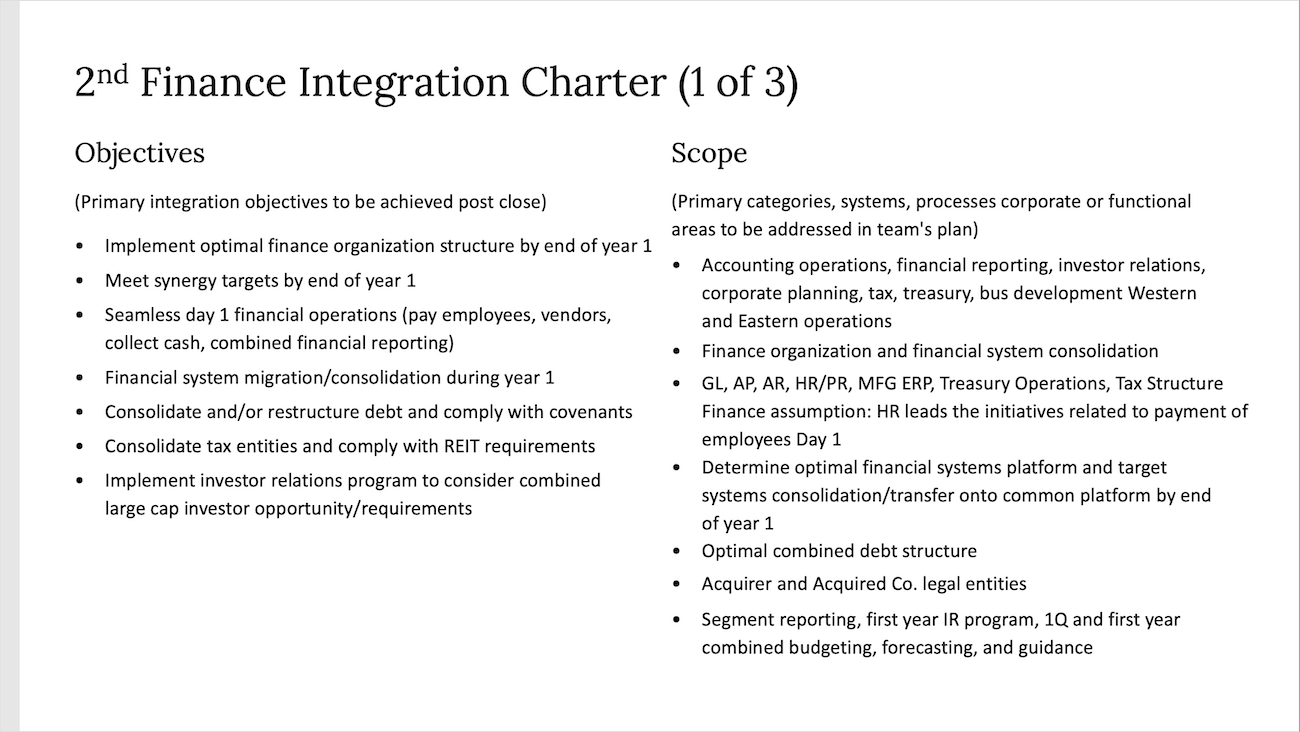

2nd Finance Integration Charter

Objectives

(Primary integration objectives to be achieved post close)

- Implement optimal finance organization structure by end of year 1

- Meet synergy targets by end of year 1

- Seamless day 1 financial operations (pay employees, vendors, collect cash, combined financial reporting)

- Financial system migration/consolidation during year 1

- Consolidate and/or restructure debt and comply with covenants

- Consolidate tax entities and comply with REIT requirements

- Implement investor relations program to consider combined large cap investor opportunity/requirements

Scope

(Primary categories, systems, processes to be addressed in team's plan)

- Accounting operations, financial reporting, investor relations, corporate planning, tax, treasury, bus development Western and Eastern operations

- Finance organization and financial system consolidation

- GL, AP, AR, HR/PR, MFG ERP, Treasury Operations, Tax Structure

Finance assumption: HR leads the initiatives related to payment of employees Day 1 - Determine optimal financial systems platform and target systems consolidation/transfer onto common platform by end of year 1

- Optimal combined debt structure

- Acquirer and Acquired Co. legal entities

- Segment reporting, first year IR program, 1Q and first year combined budgeting, forecasting, and guidance

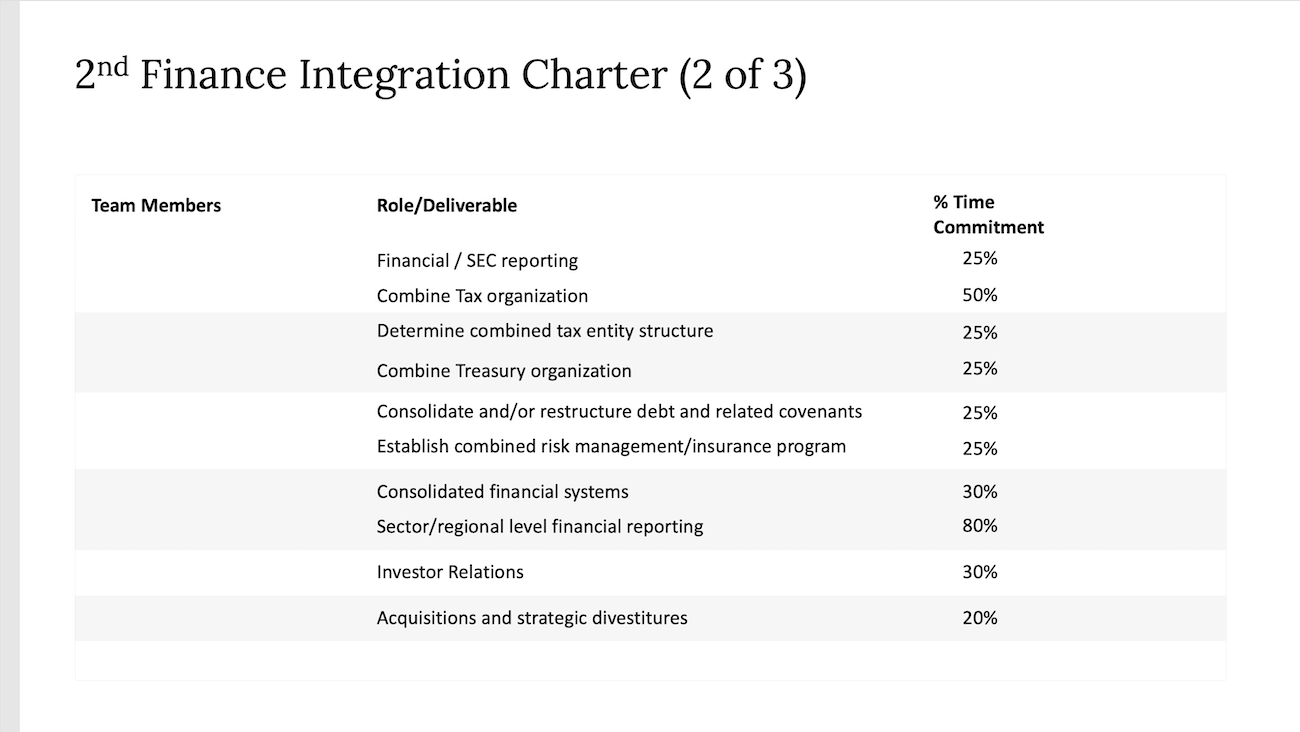

Team Members & Deliverables

| Team Members | Role/Deliverable | % Time Commitment |

|---|---|---|

| TBD | Financial / SEC reporting | 25% |

| TBD | Combine Tax organization | 50% |

| TBD | Determine combined tax entity structure | 25% |

| TBD | Combine Treasury organization | 25% |

| TBD | Consolidate and/or restructure debt and related covenants | 25% |

| TBD | Establish combined risk management/insurance program | 25% |

| TBD | Consolidated financial systems | 30% |

| TBD | Sector/regional level financial reporting | 80% |

| TBD | Investor Relations | 30% |

| TBD | Acquisitions and strategic divestitures | 20% |

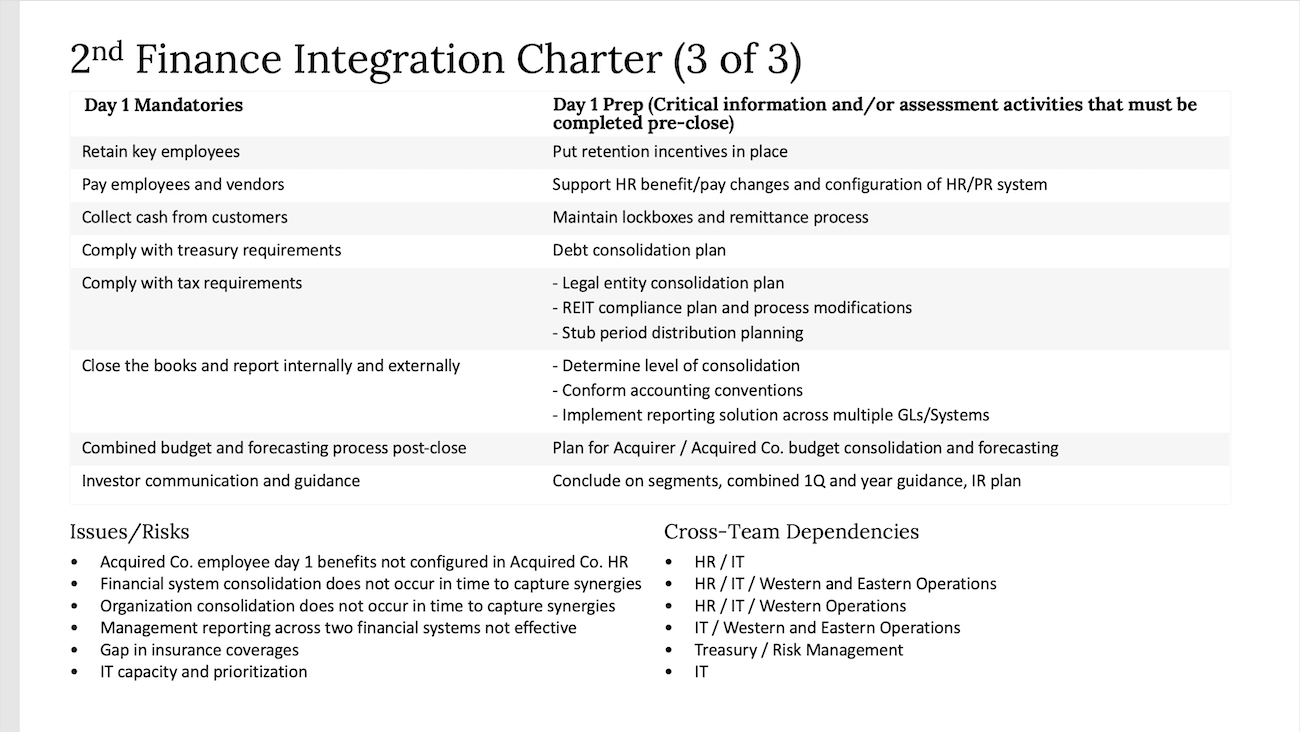

Day 1 Mandatories

- Retain key employees

- Pay employees and vendors

- Collect cash from customers

- Comply with treasury requirements

- Comply with tax requirements

- Close the books and report internally and externally

- Combined budget and forecasting process post-close

- Investor communication and guidance

Day 1 Prep (Critical pre-close activities)

- Put retention incentives in place

- Support HR benefit/pay changes and configuration of HR/PR system

- Maintain lockboxes and remittance process

- Debt consolidation plan

-

– Legal entity consolidation plan

- REIT compliance plan and process modifications

- Stub period distribution planning -

- Determine level of consolidation

- Conform accounting conventions

- Implement reporting solution across multiple GLs/Systems - Plan for Acquirer / Acquired Co. budget consolidation and forecasting

- Conclude on segments, combined 1Q and year guidance, IR plan

Issues/Risks

- Acquired Co. employee day 1 benefits not configured in Acquired Co. HR

- Financial system consolidation does not occur in time to capture synergies

- Organization consolidation does not occur in time to capture synergies

- Management reporting across two systems not effective

- Gap in insurance coverages

- IT capacity and prioritization

Cross-Team Dependencies

- HR / IT

- HR / IT / Western and Eastern Operations

- HR / IT / Western Operations

- IT / Western and Eastern Operations

- Treasury / Risk Management

- IT

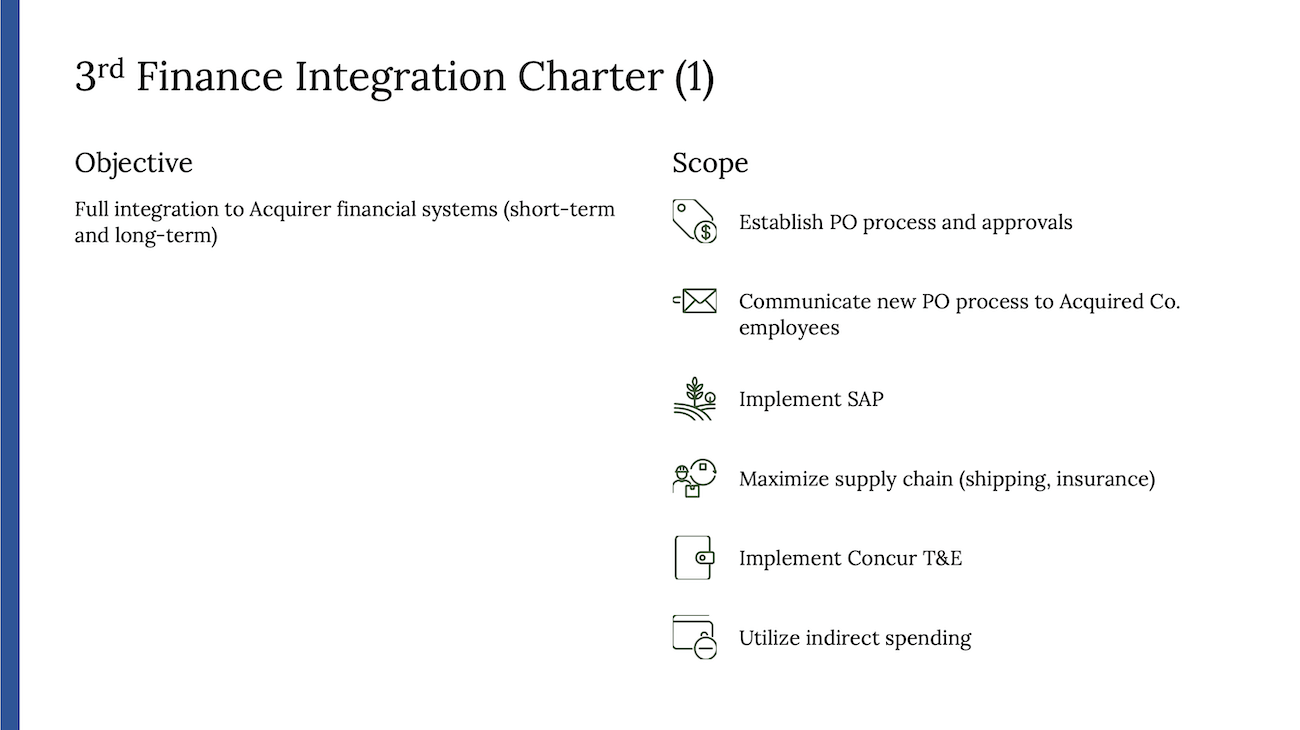

3rd Finance Integration Charter

Objective

Full integration to Acquirer financial systems (short-term and long-term)

Scope

- Establish PO process and approvals

- Communicate new PO process to Acquired Co. employees

- Implement SAP

- Maximize supply chain (shipping, insurance)

- Implement Concur T&E

- Utilize indirect spending

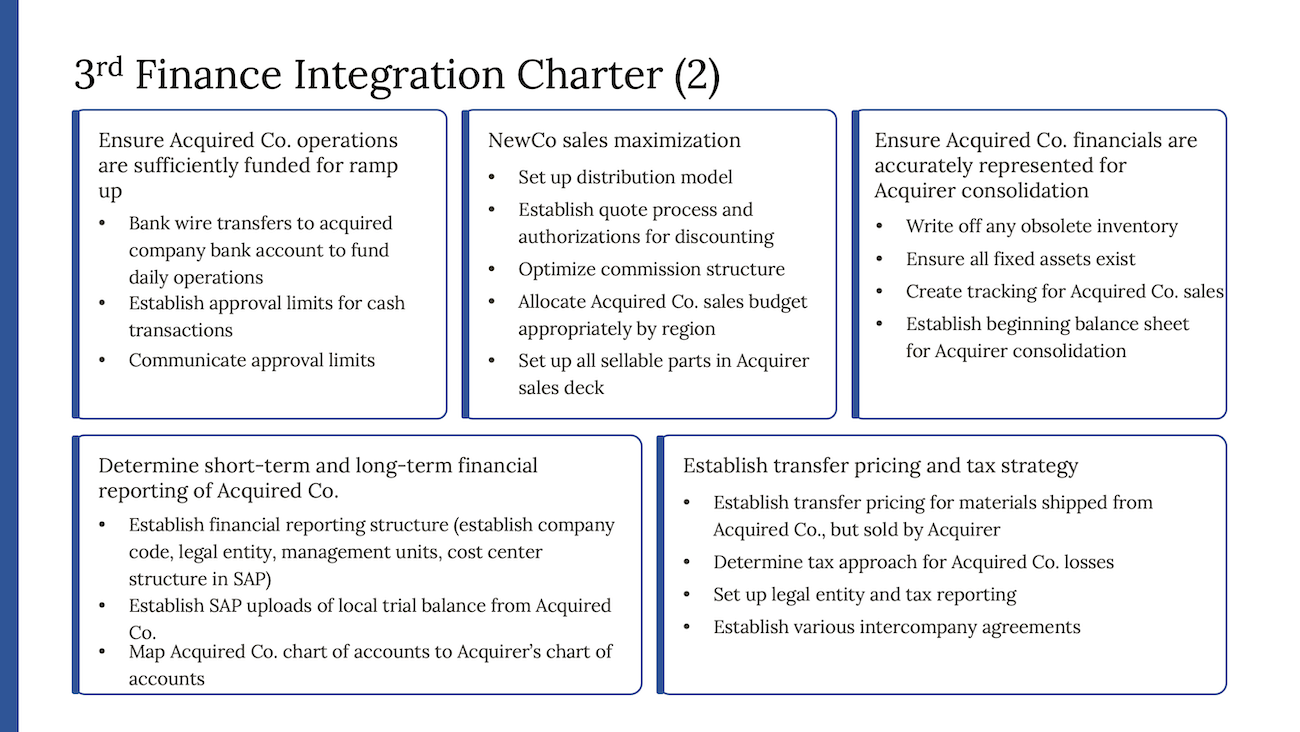

Ensure Acquired Co. operations are sufficiently funded for ramp up

- Bank wire transfers to acquired company bank account to fund daily operations

- Establish approval limits for cash transactions

- Communicate approval limits

NewCo sales maximization

- Set up distribution model

- Establish quote process and authorizations for discounting

- Optimize commission structure

- Allocate Acquired Co. sales budget appropriately by region

- Set up all sellable parts in Acquirer sales deck

Ensure Acquired Co. financials are accurately represented

- Write off any obsolete inventory

- Ensure all fixed assets exist

- Create tracking for Acquired Co. sales

- Establish beginning balance sheet for Acquirer consolidation

Determine short-term and long-term financial reporting of Acquired Co.

- Establish financial reporting structure in SAP

- Establish SAP uploads of local trial balance from Acquired Co.

- Map Acquired Co. chart of accounts to Acquirer’s chart of accounts

Establish transfer pricing and tax strategy

- Establish transfer pricing for materials shipped from Acquired Co., but sold by Acquirer

- Determine tax approach for Acquired Co. losses

- Set up legal entity and tax reporting

- Establish various intercompany agreements

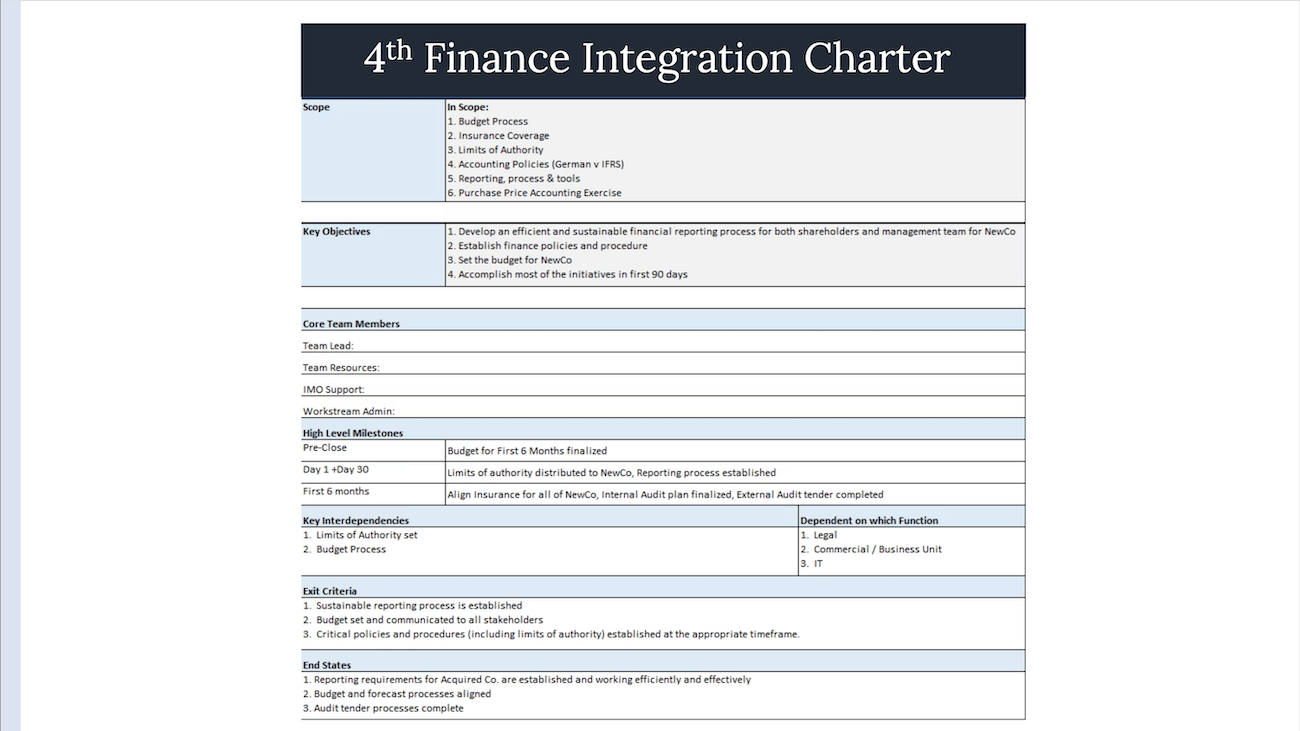

4th Finance Integration Charter

Scope

- Budget Process

- Insurance Coverage

- Limits of Authority

- Accounting Policies (German v IFRS)

- Reporting, Process & tools

- Purchase Price Accounting Exercise

Key Objectives

- Develop an efficient and sustainable financial reporting process for both shareholders and management team for NewCo

- Establish finance policies and procedure

- Set the budget for NewCo

- Accomplish most initiatives in first 90 days

High-Level Milestones

- Pre-Close: Budget for First 6 Months finalized

- Day 1 + Day 30: Limits of authority distributed. Reporting process established

- First 6 months: Align insurance for all of NewCo. Audit plans finalized.

Core Team Members

- Team Lead: TBD

- Team Resources: TBD

- IMO Support: TBD

- Workstream Admin: TBD

Key Interdependencies

- Limits of Authority set

- Budget Process

Dependent on which Function

- Legal & Admin

- Commercial / Business Unit

- IT

Exit Criteria & End States

Exit Criteria

- Sustainable reporting process is established

- Budget set and communicated to all stakeholders

- Critical policies and procedures established

End States

- Reporting requirements are established and working efficiently

- Budget and forecast processes aligned

- Audit tender processes complete

Related Presentations